Corporate Sustainable Due Diligence Directive - A focus on your entire value chain

On 23 February 2022, as part of its “Just and sustainable economy” package, the European Commission published its proposal for a Directive on Corporate Sustainability Due Diligence (“CSDDD”).

The proposal sets out a horizontal framework for companies with an EU footprint, whether based in Europe or providing goods or services into the EU, governing how they respect human rights and environment through their global value chains. It includes changes to directors’ duties and requirements for value chain due diligence.

With this proposed directive, the European Commission aims to create a union-wide transparent and predictable framework that helps companies to assess and manage sustainability risks and impacts with respect to core human rights and environmental risks across their value chains. It will respond to a lack of harmonised legal framework on corporate due diligence obligations across Europe as there was no outstanding EU legislation directly covering due diligence requirements on companies’ supply chains.

Companies will be required to identify actual or potential negative impacts from their value chain on human rights and the environment, and to take measures to mitigate those impacts. In addition, companies are required to adjust and align their business plans and strategies with the transition to a sustainable economy and the limitation of global warming to 1.5 degrees Celsius, in accordance with the Paris Agreement.

Similar efforts have also been recently undertaken by the US and the UK. In June, President Biden signed an Executive Order on supply chain resilience. The UK has stated that it will be introducing legislation shortly along similar goals as the EU are contemplating.

Complementary to the Corporate Sustainability Reporting Directive

The proposed directive is complementary and closely related to the adopted Corporate Sustainability Reporting Directive (“CSRD”) and with the EU Taxonomy’s minimum social safeguards.

Furthermore, companies that fall under the scope of both directives should report on their due diligence duties. The proposed CSDD Directive will thus lead to more complete and effective reporting under CSRD.

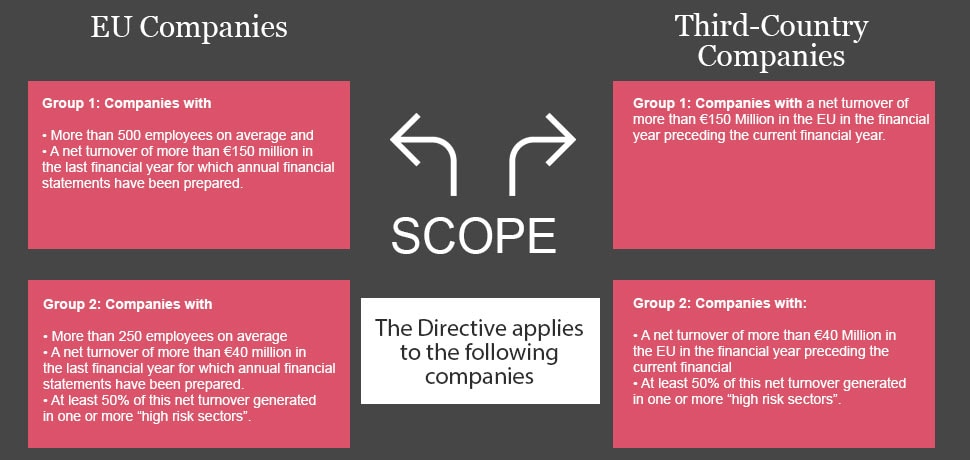

Scope

Timing

It is expected that the directive will be adopted by the EU in 2024, applicable to the first group of companies as from 2026, after the period of transposition of the Member States in the national law, while for the second group of companies, this will be applicable still 2 years later.

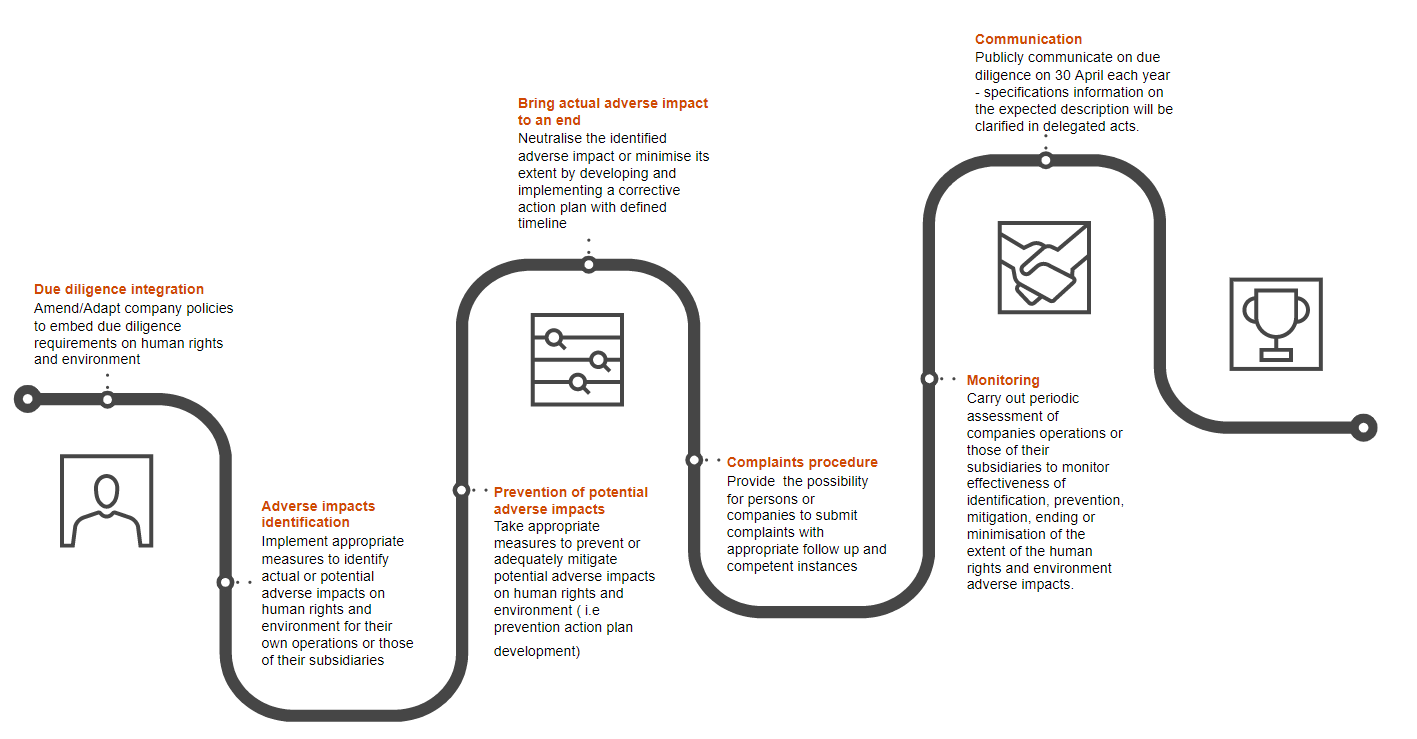

What does it imply in practice?

It builds on the UN's Guiding Principles on Business and Human Rights and OECD Guidelines for Multinational Enterprises and responsible business conduct, and is in line with internationally recognised human rights and labour standards which include due diligence measures for companies to identify and address adverse human rights impacts and to carry out environmental adverse impact assessments.

Adverse impact includes, in particular, human rights issues such as forced labour, child labour, inadequate workplace health and safety, exploitation of workers, and environmental issues such as greenhouse gas emissions, pollution, or biodiversity loss and ecosystem degradation.

Directors’ Responsibilities towards a Sustainable Economy

The Board of directors must take into account the consequences of their decisions with respect to sustainability matters, climate change and human rights, being responsible for the implementation and supervising the supply chain due diligence process.

In this context, the directive includes a link between the company’s sustainable strategy and the variable remuneration of the directors to their contribution to long-term sustainability measures and commitment.

It is essential to note that the directive will also provide for a combination of sanctions and civil liability.

Challenges

Enhance governance to tackle the requirements of the new directive

Reinforce the current internal policies in place to embed human rights and environmental risks, describe measures taken, engage with the suppliers, obtain reliable information and transform where required

Ensure appropriate data collection process for reporting purposes (availability, security, accuracy and completeness of data)

Monitor the progress towards the objectives

Adapt and align the directors’ remuneration to the climate, environment and human rights objectives and

Report on 30 April each year for the previous calendar year

Benefits of the value chain due diligence

Valuable contribution to create a sustainable and fair economy and society

Contribution to bring the sustainability reporting on par with the financial reporting

Improvement of the organisation risk assessment over the entire value chain

Decrease of reputational risks

Easier and cheaper access to financing

Consumer and employees loyalty

Competitive advantage

Planning your next steps

Do you have questions about whether the obligations of the proposed directive might apply to your company? Are you wondering how to start that journey? Feel free to contact PwC Luxembourg representatives.

Follow us