Our industries

We support our clients with services in five major industries: Alternatives, Asset and Wealth Management, Banking, Insurance and Industry & Public Sector.

Alternatives

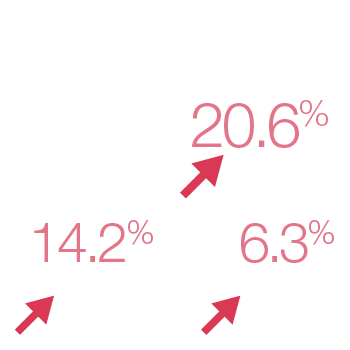

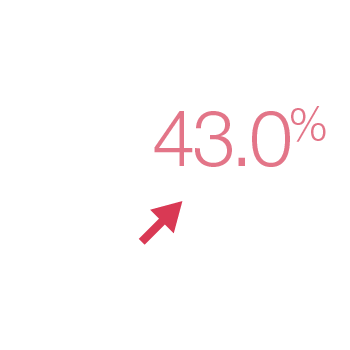

Our Alternatives industry segment experienced a strong growth (+23.2% in growth from the previous year), not only in Private Equity and Real Estate but also in the sub-industries of Private Debt and Infrastructure. As in the previous year, Alternatives was the largest revenue increase for the firm, where growth was seen across all Lines of Services, but the increase in Advisory was especially notable in relative terms (revenue more than doubled).

This industry’s success is attributed to the win of new clients and the development of an X-LoS approach for existing clients; enabling and partnering in their business growth and establishing long-term relationships. Furthermore, growth in Alternatives is attributed to the roll-out of the Managed Services offering, and also a further focus on ESG and Valuation.

In the next 12 months and beyond, the Alternatives sector will face a series of challenges but also opportunities. Many factors, including unprecedented inflation and interest rate volatility, will cause Alternative asset managers to examine deeply their business models, sectoral focus and wider purpose. Technology transformation and talent acquisition will remain the key success factors to underpin market advantage, profitability and relevance. Our firm is investing to ensure the best possible support for our clients and their success.

Asset & Wealth Management

Our Asset and Wealth Management (AWM) practice, including all our activities around traditional funds, showed a stable Turnover (+0.4% in growth from the previous year) in a highly competitive environment. We have defended the market-leading position of our Assurance practice and launched a series of innovative services focusing on ESG, Management Companies and Asset Management Digital Solutions.

A major trend is the broadening of our clients' business books beyond traditional listed securities investments towards real and alternative assets. This trend also explains the asymmetric growth patterns within our Alternatives and AWM industry segments.

Together with a series of leading asset managers, we have launched a strategic initiative to maintain Luxembourg's funds Centre as the global solution set of choice for global asset managers. Speaking with more than 30 clients, we have drafted the Luxembourg User experience in Asset Management paper.

More than ever in this digital environment, we continue helping clients to find the right solutions tailored to their needs through digital solutions like technology enabled managed services and assurance services relative to ESG.

Banking & Capital Markets

The Luxembourg banking market remains a resilient sector despite the effects of the pandemic and the current geopolitical situation. However, the months to come will certainly be interesting for banks especially with the rise of interest rates.

Once again, this year our Banking practice demonstrates strong financial results (+4.6% in growth from the previous year). Growth was mainly driven by our Advisory practice and relies on four main factors: (1) transformation and change management projects, (2) international and cross-border projects jointly with other PwC Network firms, (3) a continuation of the regulatory change and compliance agenda with focus on Anti-Money Laundering (AML) and Outsourcing, (4) rising interest in Digital/Technology transformation, which we predict will continue in the next 12 months, together with Risk related matters.

Our recent Banking Trends & Figures market analysis also highlights great opportunities for banks in the payments sector, especially when it comes to B2B and cross-border payments.

Insurance

Luxembourg’s insurance ecosystem continues to be enhanced through investments by incumbents as well as the arrival and development of newer entrants.

PwC Luxembourg’s insurance practice supports the broad base of industry actors from insurers themselves, brokers, agencies, and also banks, and asset managers with their insurance-related activities.

Our Assurance industry revenues decreased as expected due to the mandatory audit firm rotation in both 2021 and 2022. Most other areas of our business within Advisory and Tax consulting as well Actuarial & Risk modelling grew strongly. The underlying driver is the desire of insurers to further transform and modernise their businesses leading to an increased focus on key areas including technology, regulatory compliance and M&A. We expect this to remain over the coming 24 months as insurers seek to enhance their stakeholder experience and tackle inflationary pressures through technology and data-related investments. Retention and development of talents is high on the sector's agenda.

Industry & Public Sector

With a 5.3% yearly growth, the Industry & Public Sector practice achieved the second-highest performance of our firm in terms of growth rate. This achievement has contributed to the development of our client base in Assurance, where the market continues to recognise the outstanding quality of our audits and the prolonged momentum in Consulting services for the Public Sector.

In that area, the demand is fueled by a heavy EU and governmental agenda, in areas such as Public Services Modernisation (Including Digital Transformation), Borders and Customs and Healthcare, as well as Policy Advice, particularly in Sustainability and Climate Finance, Energy and Trade.

The Corporate business transformation agenda (ERP, Cloud, Data, Artificial Intelligence, Cyber) forms the other growth pillar of our Consulting practice. Additionally, our tax practice continues to be recognised as the leading provider of consulting and compliance services, helping our local and international clients navigate the ever-growing complexity of the EU/worldwide tax regulations.