Our solutions to comply with FATCA and CRS requirements

FATCA and CRS compliance

Your challenges

You must mitigate any risk of non-compliance with your FATCA and CRS obligations, but you are facing following operational challenges:

- High level of expertise needed to monitor legal updates and comply with diverse obligations

- FATCA/CRS classification and registration (if required) of your entities in different jurisdictions and correct completion of self-certification forms

- Plausibility checks of FATCA/CRS self-certification forms received from investors / clients

- Compliance with filing obligations in different jurisdictions (incl. IT systems, gathering of financial data, etc.)

- Set-up of compliance framework (incl. audit trail, performance of oversight over delegated functions, etc.)

- Communication with tax authorities and clients / investors

Our FATCA/CRS services

In order to help you reaching a full FATCA/CRS compliance, we offer you a complete range of FATCA/CRS services with our FATCA/CRS Compliance Suite of Services as well as our hotline:

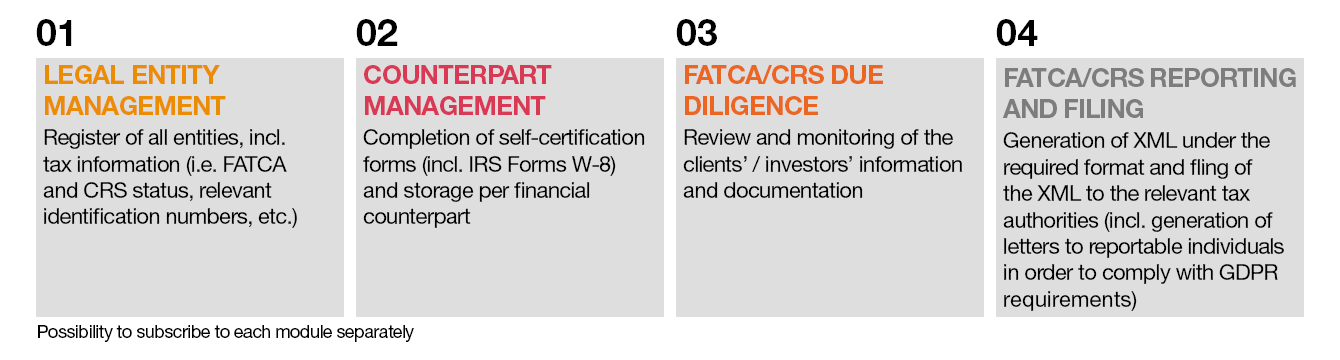

Our expert team performs an analysis of the FATCA and CRS status of an entity and helps you with the relevant local registrations and registration with the Internal Revenue Service (IRS), if required.

In addition, we can assist you with other related tax filings (such as the Form SS-4 to apply for an employer identification number (EIN) or Form 8832 for the Entity Classification Election).

We complete FATCA/CRS self-certification forms requested by your financial counterparts.

In addition, we complete U.S. withholding certificates (i.e. W-8BEN-E, W-8IMY, etc.) and prepare withholding statements to benefit from reduced US withholding tax rates.

All documentation provided to different counterparts is stored on one platform which allows you to keep track on all documentation provided to each counterpart.

We assist you with the collection of FATCA/CRS Self-Certification forms from clients / investors and perform a critical review for completeness and reasonableness. In case of a change of circumstances, we assess whether the existing documentation needs to be updated.

We prepare FATCA and CRS reports on an annual basis and file the reports with the relevant tax authorities. We perform data quality controls and reconciliations. Based on the data included in the reports, we can generate notifications letters to reportable individuals to inform clients / investors about their personal data that will be exchanged.

We can assist you with the drafting of FATCA/CRS procedures, processes and controls (incl. audit trail and oversight), taking into consideration best market practice.

We can also provide you with ad hoc advice regarding questions arising during your day-to-day operations in the form of a hotline.

Full FATCA/CRS compliance

Our FATCA/CRS Compliance Suite of services

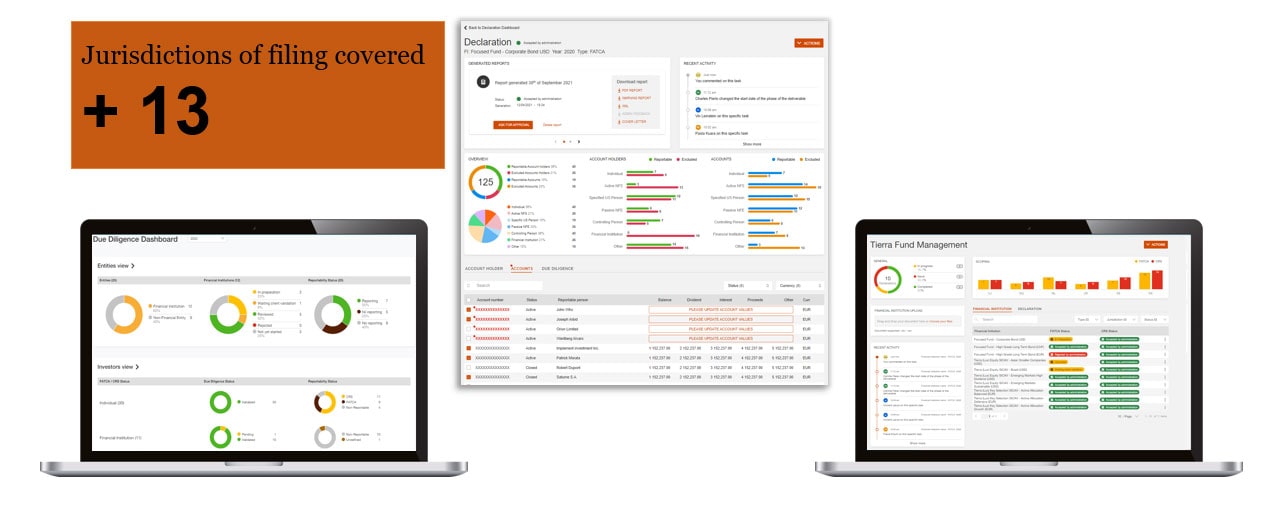

- We have developed a web-based operational solution which allows you to monitor FATCA and CRS compliance at group, entity and client / investor level.

- Our collaborative solution enables you to have a centralised view of the FATCA and CRS obligations of all entities in your jurisdictions in scope.

- Your oversight is documented in an audit trail.

Our services are supported by innovative and secure digital solutions with extensive market coverage and constantly updated with market changes.