Principal Adverse Impact Statements in the AWM Industry

Mind the Gap

Our new report "Mind the Gap: Principal Adverse Impact Statements in the AWM Industry", is an in-depth study, the first of its kind, conducted on the Principal Adverse Impact (PAI) disclosures.

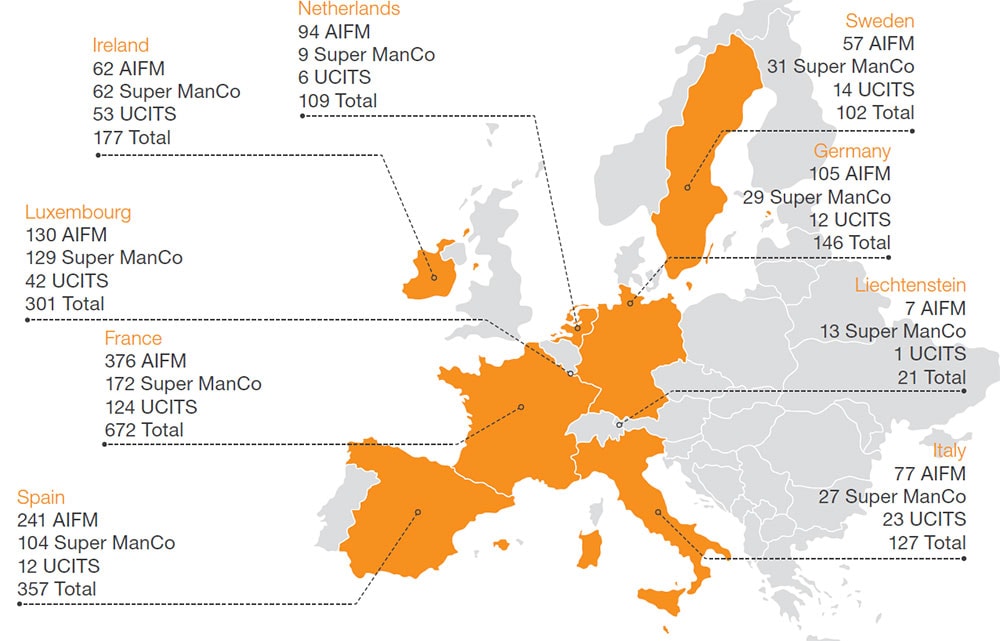

We analysed two-thirds of the total 3,212 management companies (ManCos) registered either with a UCITS (UCITS ManCo), Alternative Investment Fund (AIFM), or both licenses (Super ManCo) with the European Securities and Markets Authority (ESMA)

Management Companies in Scope of Our Study

Only one in five management companies publicly disclosed a Principal Adverse Impact statement in 2022

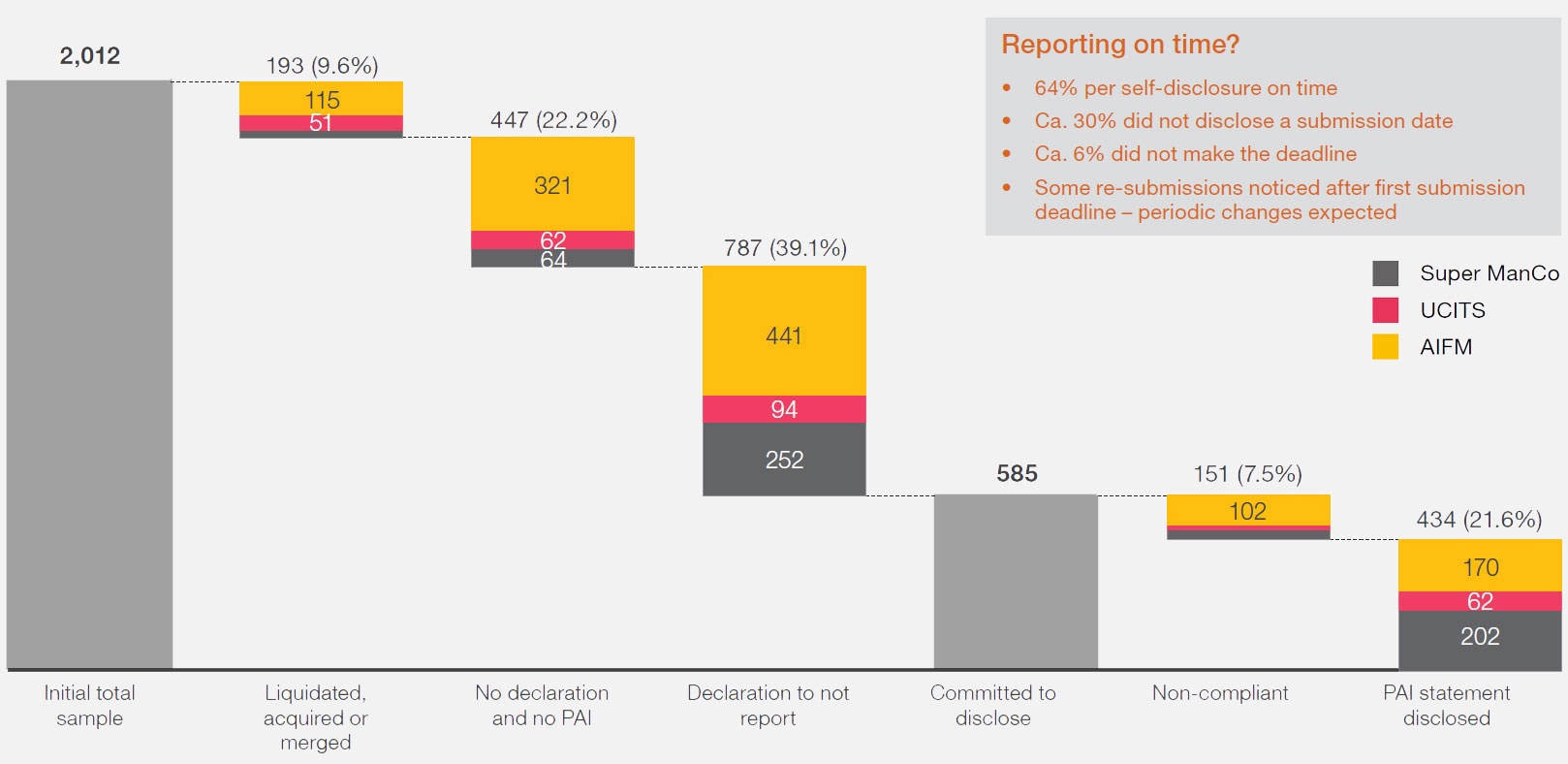

The report shows that only 21.6% of the management companies (‘ManCos’) in the scope of the study issued a publicly accessible Principal Adverse Impact (PAI) statement. Of the issued statements, just over one in five (21.9%) followed the template prescribed by the Sustainable Finance Disclosure Regulation (SFDR)’s Regulatory Technical Standards (SFDR Level II), resulting in significant disparities with limited data comparability.

Our study also found that 22.2% of the firms surveyed were not compliant with the regulations, in other words neither published a PAI statement nor a declaration on why they would not report on PAIs at entity level. A further 7.5% of companies, while they had committed to disclosing the data, were not compliant with SFDR Level II.

We reviewed data from 2,012 management companies across nine European countries, accounting for 62.6% of the total number of UCITS ManCos, AIFMs, and Super ManCos registered with ESMA, finding wide variations in the quality and substance of publicly available PAI statements. While there were positive examples, the majority of published statements were incomplete, lacked quantitative- and qualitative-rich insights, or in some instances were left entirely blank.

In addition, 39.1% of the firms surveyed declared they did not consider the PAIs of their investment decisions on sustainability factors, with the most frequently observed reasoning being insufficient availability of satisfactory and pertinent non-financial data, as well as uncertainties regarding the data collection methods required.

Breakdown by licenses on reporting classification

Ensuring better compliance

The report presents a series of recommendations for firms to ensure better compliance and alignment with regulators’ expectations in future PAI statements, including the systematic usage of the template provided by the European Supervisory Authorities, methodology and data management, as well as highlighting the benefits of accurate PAI reporting for investors. On the other hand, improvements in the structure, completeness, ease of use and prescribed electronic format of the current reporting template would provide a substantial input in easing the challenges for firms and comparability of the statements prepared. This would increase the usefulness for interested stakeholders.

"Sustainability regulations are only going to continue to expand in scope and complexity in the coming years. Our analysis shows much work remains to be done if PAI statements are to play a pivotal role in informing stakeholders about investments’ adverse impacts on sustainability and progressing sustainable investments. To achieve this, management companies need to ensure they have reliable and technologically-advanced data collection mechanisms to efficiently track progress, alongside a systematic methodology with well-defined benchmarks."

Olivier Carré, Deputy Managing Partner, Technology & Transformation Leader

"PAI statements are the first step for many firms into sustainability reporting and may provide relevant actionable insights for stakeholders into what impacts firms’ investment decisions have on sustainability factors.

Expected growing pains are clearly evident as:

- the required sustainability information is in many instances not easily accessible or available at all from the invested companies;

- for reported PAI results it is in general unclear what controls and quality management measures were put in place;

- the reporting template required to be used by the firms is currently not designed to ensure comparability for reported results between firms as practices differ significantly. This is why we have developed our proprietary scoring model, the PwC PAI Transparency Score Card, which tracks compliance, completeness and transparency of PAI disclosures, to support improved future benchmarking on entity level.”

Michael Horvath, Partner and Regulatory Advisor

Mind the Gap

Principal Adverse Impact Statements in the AWM Industry

Contact us

Olivier Carré

Deputy Managing Partner, Technology & Transformation Leader, PwC Luxembourg

Tel: +352 49 48 48 4174

Dariush Yazdani

Partner, Global AWM Market Research Centre Leader, PwC Luxembourg

Tel: +352 49 48 48 2191