"There is no alternative" – a sentence that emerged in the mid-19th century and which found its way into common political and economic parlance, reflecting the commonly-held conviction that inaction is not an option, even in a world of imperfect alternatives. What if we applied TINA to the environmental, social and governance (ESG) paradigm that has been shaping the global asset and wealth management (AWM) industry? Regardless of one’s views and hesitations on ESG – whether its benefits ultimately outweigh its costs – one thing is clear: ESG is here to stay, as both the AWM industry and policymakers appear set on an irreversible course of action.

Bolstered by a change in policy, important shifts in societal expectations, and the ever-increasing sophistication of regulatory rules, ESG considerations today represent an important characteristic of a material number of global Asset Management products and investment strategies. This has seen Global ESG Assets under Management (AuM) skyrocketing more than eight-fold since 2015, surging at an impressive 42.7% CAGR to reach USD 18.4tn as of end-2021.

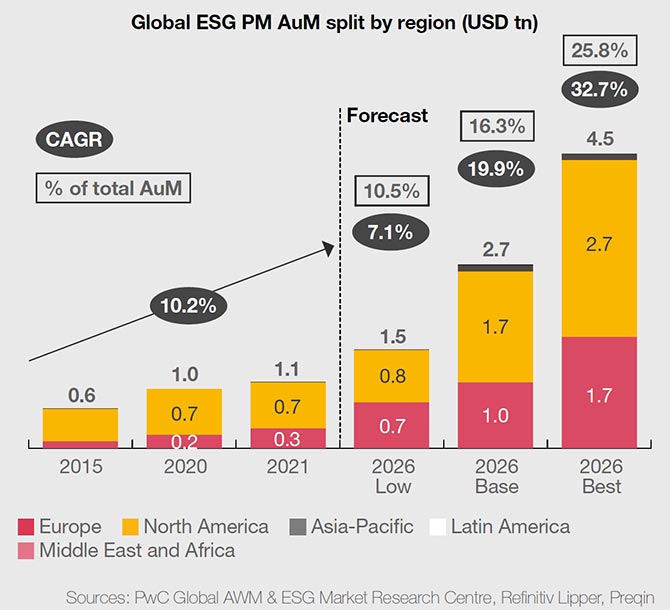

While this seismic transition has been largely driven by the world’s public markets, Private Markets (PM) have not stood idly by. An all-encompassing reboot saw ESG PM AuM nearly double since 2015, as the industry’s stakeholders attribute an unprecedented degree of importance to sustainability considerations. Today, ESG represents an unyielding focal point of the global PM landscape and is set to rapidly transform it. Our forecasts attest to this anticipated growth, with Global ESG PM AuM poised to surge between two- and four-fold according to a base- and best-case forecast scenario.

About our European Sustainable Finance Series and this report

Since 2020, our European Sustainable Finance Series has been offering surveybacked perspectives on the era-defining opportunity that ESG represents for Asset Managers across Europe's public and private market landscapes. Across the three reports published to date, we have taken stock of the key trends propelling the 'ESG shift' across the region's mutual funds, private markets and fixed income industries – formulating key actions that the Managers operating in these spaces should consider taking in order to seize the ESG opportunity with both hands.

Given the rate and scale with which the ESG paradigm shift has expanded into a truly global trend since the start of this series, this report – the fourth of the series – will take a deep dive into how regulation has driven the ESG uptake across the EU, UK, US and APAC. Specifically, we will take stock of the past, present and expected regulatory developments of each region, delving into how these are perceived by LPs and GPs in each jurisdiction, as well as the challenges created, the opportunities unlocked, and the changes required.

We use our findings to make informed recommendations as to the key actions that General Partners should consider in order to navigate the changing ESG landscape and unlock the opportunities it presents. We have further enhanced our report based on a wide range of primary data gathered through a survey of 300 GPs and 300 LPs across all four jurisdictions.

Region-specific ESG disclosure standards & challenges: Overview

Given the rapid and global nature of this ESG shift, regulators have taken varying approaches towards tackling ESG issues, both in terms of urgency and strategy. This has resulted in a lack of uniformity in disclosure regulations and standards across different regions and jurisdictions, with each at a different stage of their respective sustainability journeys. As a result, LPs and GPs are encountering region-specific challenges and opportunities.

To gain insight into the various ESG reporting practices, requirements, and challenges faced by LPs and GPs, we have conducted a survey to identify the varying approaches taken by different entities in the ESG reporting space and help develop a better understanding of the current ESG landscape.

European Union

Policymakers in the EU have strongly positioned themselves as the flag-bearers of ESG regulations, taking the lead globally through the development of actionable plans aimed at embedding sustainability considerations within the region’s financial services landscape. The strong regulatory and legislative momentum behind ESG has cemented the EU as the global frontrunner in the ESG space, alone accounting for 69.5% of global ESG assets as of end-2021.

The issuance of the EU “Action Plan on Financing Sustainable Growth” in March 2018 marked a major move towards solidifying Europe as the global centre for sustainable finance, taking the ESG decision out of managers’ hands, requiring them to quantify and elucidate the ESG impacts of their investments – whether positive or negative – to their investors. In doing so, the EU is catalysing the transition towards a sustainable standard for investing, stimulating a surge of ESG adoption within the investment processes of European-operating managers.

The Action Plan introduces three overarching landmark regulations which focus on establishing a framework through which investors and regulators will be able to determine the degree to which economic activities follow ESG standards: The Sustainable Finance Disclosure Regulation (SFDR), the EU Taxonomy, and the Corporate Sustainability Reporting Directive (CSRD) – all three of which directly impact LPs and GPs.

As a whole, the Action Plan will shape the opportunities, risks and threats that Asset Managers will face in the coming years, setting the foundation upon which all future EU – and possibly global – sustainable finance regulations are built.

United Kingdom

Since its departure from the EU in 2020, the United Kingdom has signalled its intention to establish itself as a global sustainable finance leader, setting ambitious net-zero targets and integrating ESG considerations into its regulatory framework. This has led to a significant ESG shift in the country's regulatory landscape – with new initiatives and regulations being launched to promote greater transparency, accountability, and sustainability in the UK financial sector.

The UK's independent ESG journey post-Brexit began with the 2019 Green Finance Strategy. This strategy was launched by the UK government to mobilise investment towards a sustainable economy and address climate change. The strategy recognised the importance of ESG factors in investment decisions and set out a roadmap for the UK to become a world leader in green finance. This strategy was a crucial step towards embedding ESG considerations into the UK's post-Brexit financial landscape and demonstrating the country's commitment to sustainability.

November of the following year saw the unveiling of the UK government’s “Roadmap towards mandatory climate-related disclosures”, in which it announced its intention to make TCFD-aligned disclosures mandatory across the economy by 2025.

October 2021 saw the UK government intensify its transitionary efforts through the announcement of its “Greening Finance Roadmap,” which shifts the focus of the ESG disclosure regulation towards the country’s financial services sector. The roadmap encompasses various measures such as raising disclosure requirements, introducing new green finance products, and establishing sustainability standards for investments. The roadmap included the introduction of two pivotal pieces of ESG disclosure regulation, the UK Green Taxonomy and Sustainable Disclosure Requirements (SDR).

United States

While the last decade has seen Asset Management stakeholders in the US become increasingly cognisant of the detrimental impact climate change can have on the industry, resulting in the launch of a number of voluntary disclosure and reporting standards, the US is taking a notably more cautious approach to ESG regulations when compared to the EU and the UK. Several factors – such as political opposition to ESG and a lack of consistent regulation at the federal level – contributed to this disparate approach.

That being said, while the US is still a nascent player in the ESG space, there have been some recent developments that could see the country catching up with its European counterparts. In 2022, the SEC proposed several new rules which – if finalised – could significantly impact the way public companies and Asset Management stakeholders approach ESG issues in the US, help drive accountability and transparency, and ultimately strengthen the sustainable finance landscape of the US.

Asia Pacific

Although ESG investing in the APAC region still lags behind Europe and North America, there is no denying that the momentum is there – with APAC-domiciled ESG AuM skyrocketing five-fold from USD 0.2tn in 2015 to over USD 1tn in 2021.

This growth in ESG investing has been met with a strong pickup in regulatory momentum among policymakers in the APAC region. Indeed, in recent years, several countries have taken major strides towards integrating ESG considerations within the region’s Asset Management markets and regulatory frameworks. The number of voluntary and mandatory ESG regulations aimed at the region’s Asset Managers and Asset Owners has surged over the last decade, skyrocketing almost seven-fold between 2014 and 2021 and almost doubling in the last five years alone.

Progress is not only being made on a country-specific level. Within the 11-country Association of Southeast Asian States (ASEAN), important region-wide initiatives have come to the fore to enhance transparency and objectivity in the markets, such as the ASEAN Taxonomy and the ASEAN Sustainable and Responsible Fund Standards. Different Taxonomies have also been developed with the aim of standardising sustainability-related definitions. As of October 2022, more than 10 different Taxonomies have been implemented or are under development among APAC countries.

Key actions: Navigating the sustainability disclosure & data landscape

In light of the above, LPs across the world have been increasingly focusing on ESG considerations across the different PM asset classes, while GPs who fail to adapt to changing investor demands risk losing business from the fast-increasing number of increasingly ESG-oriented investors.

Here are some of the key actions that LPs and GPs active in the Private Markets landscape should consider when embarking on their ESG journey.

Reassess your deal sourcing and due diligence

The holistic integration of ESG considerations throughout the investment life cycle is essential for realising ESG’s potential value creation and protection opportunities while aligning with evolving regulatory demands and LP expectations.

This integration requires structural changes. With this in mind, we have identified three crucial steps that GPs should consider taking to incorporate ESG considerations throughout their investment life cycle.

Rethink your risk management and reporting procedures

As ESG becomes an increasingly central facet of the regulatory landscape, GPs are being encouraged to reevaluate their risk management processes to incorporate non-financial risks alongside financial ones. In this new backdrop, it is no longer sufficient to prioritise financial risk at the expense of non-financial risk. It is crucial to recognize that non-financial risks, such as environmental and social risks, can have a significant impact on the long-term financial performance of a portfolio company.

Upskill your workforce

As ESG considerations become increasingly entrenched in the operational DNA of Asset Managers across the globe – and as regulator and investor expectations mount – it is becoming increasingly crucial for GPs to deepen and integrate their ESG capabilities across their organisations. To successfully transition towards an ESG-driven approach, it is essential to cultivate a diverse and skilled talent pool that can bring fresh perspectives and support the organisation's transitionary efforts. This entails acquiring a broad range of practical and qualitative skills, such as ESG data/analytics, risk analysis, impact analysis, and policy monitoring

Manage the transition and timing

As long-term investors, alternative fund managers and GPs have always considered turnaround management, until now mostly focused on financial KPIs, as a core strategy for value creation. With the importance and valuation impact of non-financial metrics and performance, the management of these dimensions in terms of ‘transition’ is creating a major opportunity for value creation, but also a major threat if not properly managed, up to the material loss of value.

Upgrade your data collection & analysis capabilities

Successfully implementing the aforementioned action points requires mastering the data challenge. Timely, accurate, and relevant data is crucial not only for achieving regulatory compliance but also for effectively quantifying ESG-related risks and improvements. This, in turn, provides a quantifiable basis for assessing ESG's potential for value creation

Contact us

Olivier Carré

Deputy Managing Partner, Technology & Transformation Leader, PwC Luxembourg

Tel: +352 49 48 48 4174

Partner, Global Sustainability Markets Leader, PwC Netherlands

Tel: +31 (0)62 248 81 40

Tarek Shoukri

Private Equity, and Sovereign Investment Funds Strategy and M&A Advisory, PwC Middle East

Tel: +971 4 304 3100

Partner, Global AWM Market Research Centre Leader, PwC Luxembourg

Tel: +352 49 48 48 2191