A glimpse of the Securitisation Survey findings

The asset classes observed by our participants over the past year show no major surprises, with responses remaining consistent with those of the previous year. Trade receivables continue to be the most frequently mentioned asset class, even seeing a 4% increase compared to last year. This is followed by securitisation real estate products (including mortgage loans), performing loans (also up by 4% from the previous year), and bond and fund repacks. Lease receivables securitisations also faced a decrease compared to last year, with around 4% less.

Structured products continue to hold a significant place in the Luxembourg securitisation market. These products typically do not meet the criteria of securitisation under the EU Securitisation Regulation 2017/2402.

When it comes to securitisation of crypto assets, as reported in the prior year market survey, we still don’t see a notable appetite for it, and they are almost not present in the Luxembourg market (or at least not in our respondents’ portfolios).

What are the Top 5 asset classes you observed in the last 12 months?

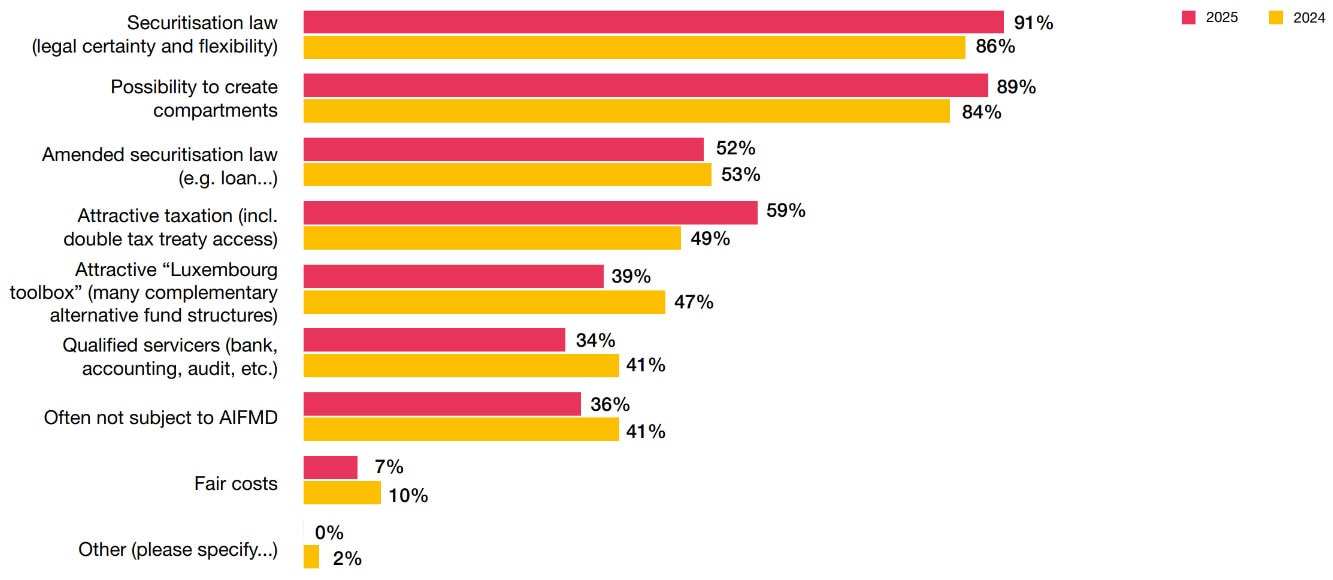

Luxembourg competitive advantage and challenges

According to our respondents, the key advantage of Luxembourg remained the legal certainty and the ability to create distinct and segregated compartments, as provided by the Luxembourg Securitisation Law. This is confirmed by the widespread use of multi-compartment vehicles. The favourable tax environment ranked third in the responses (increasing by one rank compared with prior year), while the 2022 modernisation of the Securitisation Law came in fourth.

One notable shift compared to last year’s responses regarding the challenges of setting up securitisation vehicles in Luxembourg is the change in perception of the uncertainty surrounding the application of the interest limitation rules under ATAD 1. While it remains in the top five concerns, it has moved from being the most problematic issue to the fourth position. This shift is attributed to the introduction of the single company group exemption in Luxembourg, which was approved by the Luxembourg Government in December 2024 and applied retroactively from 1 January 2024. Under these new rules, most securitisation companies are no longer negatively impacted by the interest limitation provisions of ATAD 1.

In your opinion, what attracts arrangers for setting up a securitisation vehicle in Luxembourg?

Securitisation in Luxembourg

PwC Market Survey 2025