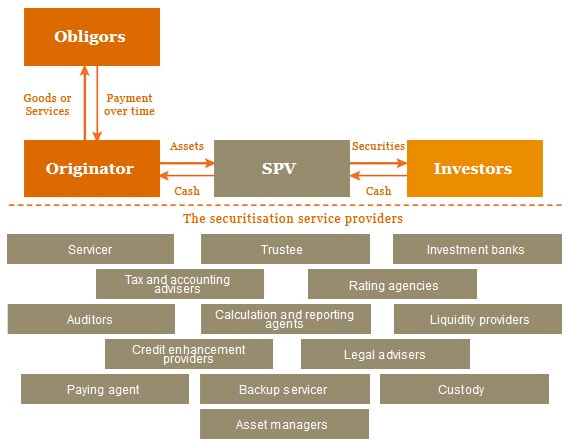

Parties involved in securitisation transactions

Securitisation provides a number of benefits for each party involved. As securitisation transactions are complex structured financing methods it is critical that potential issuers understand the range of options and related implications to reach informed decisions. Investors enjoy securities that are relatively stable, offer a good return on investment and are often guaranteed by a third party. While benefits have varying degrees of importance for different originators, the common characteristic of securitisation is the demand for lower capital cost.

Obligors owe the originator payments on the underlying loans / assets and are, therefore, ultimately responsible for the performance of the issued securities. As obligors are often not informed about the sale of their payment obligation, the originator, in many cases, maintains the customer relationship as servicer.

The Originator is the entity that assigns assets or risks in a securitisation transaction. Usually it is the party (lender) who originally underwrote and securitised the claims (loans). The obligations arising with respect to such loans are, therefore, originally owed to this entity before the transfer to the SPV takes place. Occasionally, the originator may be a third party who buys the pool with the intention to securitise it thereafter; in that case, the originator is also named as sponsor. Originators include captive financial companies of the major car manufacturers, other financial companies, commercial banks, building societies, manufacturers, insurance companies and securities firms.

Investors buy the securities issued by the SPV and are, therefore, entitled to receive the repayments and interests based on the cash flow generated by the underlying assets. Collaterals ensure the pecuniary claims from these assets. The largest investors in securitised assets are typically pension funds, insurance companies, investment fund managers, and to a lesser degree, commercial banks. The most compelling reason for investing in Asset-Backed Securities is their higher rate of return relative to other assets of comparable credit risk.

The securitisation service providers

- Servicer

- Trustee

- Investment banks

- Tax and accounting advisers

- Rating agencies

- Auditors

- Calculation and reporting agents

Servicer

The servicer is the entity that collects principal and interest payments from obligors and administers the portfolio after transaction closing. Regularly the originator acts as servicer, although this is not always the case. For example, in most Non-Performing Loans (NPL) transactions, specialised servicers tend to carry out this role. Servicing includes customer service and payment processing for the obligors in the securitised pool and collection actions in accordance with the pooling and servicing agreement. Servicing can also include default management, collateral liquidation and the preparation of monthly reports. The servicer is typically compensated with a fixed servicing fee.

Trustee

Acting in a fiduciary capacity, the trustee is primarily concerned with preserving the rights of investors. The responsibilities of the trustee will vary from one case to the next and are described in a separate trust agreement. Generally, the trustee oversees the receipt and disbursement of cash flow as prescribed by the indenture or pooling and servicing agreement and monitors compliance with appropriate covenants by other parties to the agreement. If problems occur in the transaction (e.g. defaults), the trustee focuses particular attention on the obligations and performance of all parties associated with the securities issued, particularly the servicer and the credit enhancer. Throughout the life of the transaction, the trustee receives periodic financial information from the originator/servicer delineating amounts collected, amounts charged off, collateral values, etc. The trustee is responsible for reviewing this information and ensuring that the underlying assets produce adequate cash flow to serve the securities issued. The trustee is also responsible for declaring default or amortisation events.

Investment banks

Investment banks mainly perform structuring, underwriting and marketing of the securitisation transaction.

Tax and accounting advisers

These advisers provide assistance on the accounting and tax implications of the proposed structure of the transaction. Usually, issuers aim to choose structures that will allow minimising the tax impact on the securities issued

Rating agencies

Usually, the securities issued are assessed by a rating agency to allocate a rating to them. A wide range of investors require a minimum rating of investment grade or higher. The rating process is currently dominated by the rating agencies: Standard & Poor's, Moody's, Fitch or Dominion Bond Rating Service. They use their accumulated expertise, data and modelling skills to assess the expected loss of debt securities issued by the securitisation vehicle. In general, rating agencies review the following factors:

- Quality of the pool of underlying assets in terms of repayment ability, maturity diversification, expected defaults and recovery rates;

- Abilities and strengths of the originator / servicer of the assets;

- Soundness of the transaction's overall structure, e.g. timing of cash flow (or mismatch) and impact of defaults;

- Analysis of legal risks in the structure, e.g. effectiveness of transfer of title to the assets;

- Ability of the asset manager to manage the portfolio;

- Quality of credit support, e.g. nature and levels of credit enhancements.

Auditors

In Luxembourg the annual accounts of securitisation vehicles have to be audited by one or more independent auditors ("Réviseurs d'entreprises agréés").

Calculation and reporting agents

This entity calculates the waterfall principal and interest payments due to creditors and investors.

- Liquidity providers

- Credit enhancement providers

- Legal advisers

- Paying agent

- Backup servicer

- Custody

- Asset managers

Liquidity providers

Liquidity providers are usually banks which provide the SPV with necessary cash to avoid any unsteadiness of the cash flow to the investors. It is a kind of bridge loan and short-term financing and it is not used for defaults within the underlying asset portfolio.

Credit enhancement providers

Credit enhancement is used to improve the credit rating of the issued securities. Therefore, credit enhancement providers are third parties that agree to elevate the credit quality of another party or a pool of assets by making payments, usually up to a specified amount. This is done in the event that the other party defaults on its payment obligations or should the cash flow generated by the pool of assets be less than the amounts contractually required due to defaults of the underlying obligors.

Legal advisers

As the legal structure and legal opinions are crucial to securitisation, considerable legal work goes into documentation. A typical transaction would involve numerous documents: sale and purchase agreements, offering documents, etc.

Paying agent

The paying agent is the bank that has agreed to settle the payments on the securities issued to investors. Payments are usually made via a clearing system.

Backup servicer

In case original servicers default, the backup servicer replaces them. They take over all the responsibilities allocated to the servicer.

Custody

The custodian bank is responsible for the safekeeping of liquid assets and of transferable securities of the securitisation vehicle, including the pool of assets transferred in case of true sale transactions.

Asset managers

Asset managers are responsible for selecting underlying assets, monitoring the portfolio and, if foreseen, replacing underlying assets. They are common in CDO / Structured Credit transactions.

Benefits

Benefits for originators

- Provide efficient access to capital markets

- Minimise issuer-specific limitations on ability to raise capital

- Convert illiquid assets to cash: assets that are not readily sellable may be combined to create a diversified collateral pool funded by notes issued by a securitisation vehicle.

- Diversify and target funding sources, investor base and transaction structures

- Raise capital to generate additional assets or apply to other more valuable uses

- Raise capital without prospectus-type disclosure

- Generate earnings

- Complete mergers and acquisitions, as well as divestitures, more efficiently

- Transfer risk to third parties

- Lower capital requirements for banks and insurance companies

Benefits for Investors

- Broad possible combinations of yield, risk and maturity

- Tailored sources of investments

- Portfolio diversification

- Higher returns

Benefits for borrowers

- Better credit terms

Related content

Follow us