Investment firms directive and regulation (IFD & IFR)

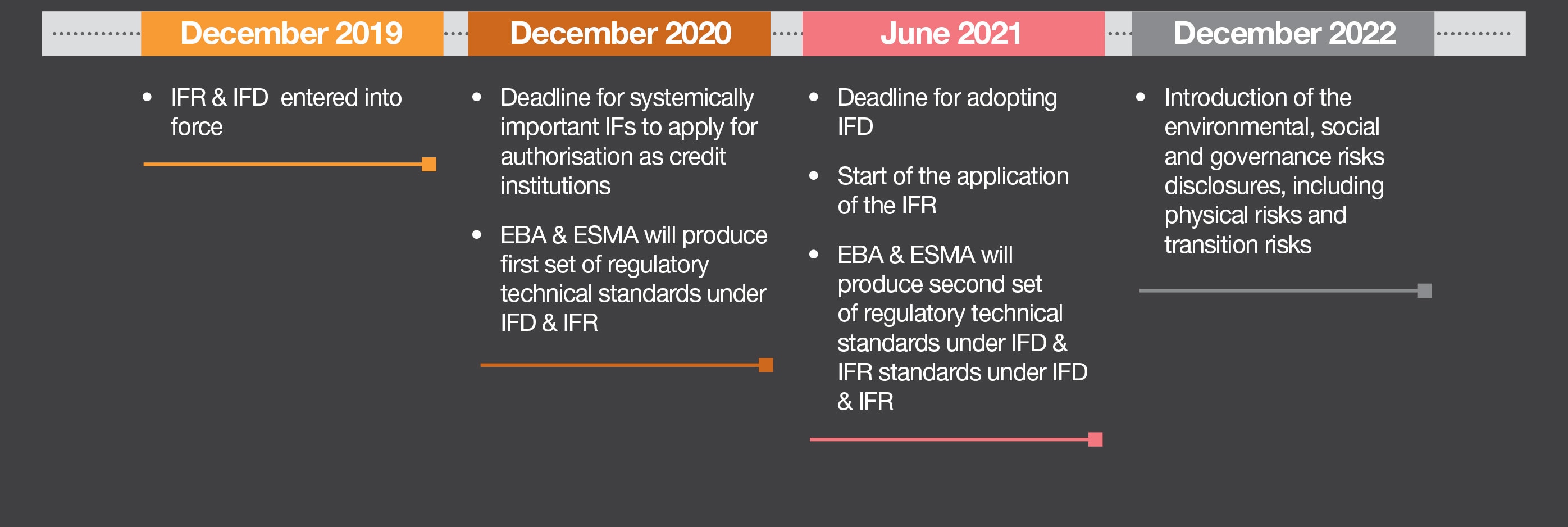

On December 5, 2019, the Directive (EU) 2019/2034 and Regulation (EU) 2019/2033 on the prudential requirements of investment firms (IFD & IFR) were published and the implementation timeline starts as from 26 June 2021.

The new regime introduces a new approach to the calculation of the regulatory capital requirements and for most of the investment firms it will result in increased capital needs, subject to transitional phasing-in. Also, new liquidity requirements, remuneration rules, internal governance, disclosure and reporting requirements will be introduced. This new framework was designed and specifically tailored to the business models of the investment firms.

Implementation timeline

On 26 June 2021 the IFR is directly applicable in all Member States and the IFD should be transposed in the local law on the same date, with the exception to the environmental, social and governance (ESG) risks disclosures, including physical risks and transition risks, which are delayed to 26 December 2022. Capital requirements are subject to a 5 year phase-in period.

A significant number of mandates was given to the European Banking Authority (EBA), often in consultation with the European Securities and Markets Authority (ESMA).

Classification of investment firms

The population of the investment firms will be split into 3 classes according to their size and complexity and each will be subject to a specific prudential framework:

Class 1

«Systemic and bank-like» investment firms

Prudential framework: CRD/CRR

Class 2

Residual category

Prudential framework: full scope IFR/IFD

Class 3

Small and non-interconnected investment firms (SNIF)

Prudential framework: limited scope IFR/IFD

New prudential framework

The IFR / IFD prudential framework includes the following elements:

- Pillar 1 requirements include minimum regulatory capital, liquidity buffer and concentration risk limits (Class 3 firms will be partially exempted from some of the elements).

- Pillar 2 capital add-ons based on ICAAP / ILAAP and SREP (very limited application to Class 3 firms).

- Pillar 3 disclosure and reporting requirements (scope and frequency of the reporting differs for Class 2 and Class 3 firms, the latter are also subject to limited disclosure obligations).

- New remuneration framework and internal governance principles (not applicable to Class 3 firms).

Regulatory reporting requirements

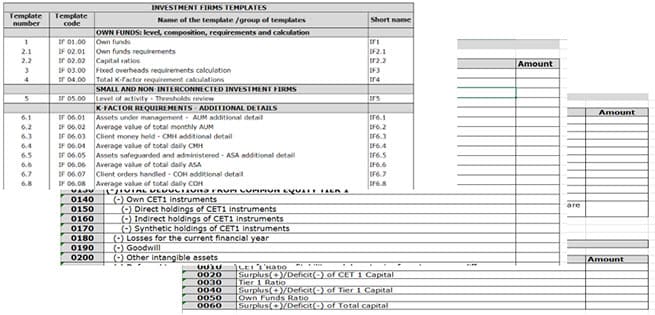

The IFR has introduced new reporting requirements for the Class 2 and 3 Investment Firms.

The European Banking Authority (EBA) was mandated to develop reporting instructions and templates as well as XBRL taxonomy, Data Point Model (DPM) and validation rules. The Reporting Framework 3.1, including ITS on reporting and disclosures for investment firms, entered into force as from 30 September 2021.

On 1 October 2021, CSSF published the revised reporting requirements for the investment firms, encompassing:

- Circular CSSF 21/784 Periodic prudential reporting of investment firms

- Updated Reporting Handbook for Investment Firms

First reporting to be prepared:

As at 30 September 2021 for Class 2 investment firms (due by 11 November 2021)

As at 31 December 2021 for Class 3 investment firms (due by 11 February)

The Class 2 investment firms will have a quarterly reporting obligation, while the Cass 3 firms would need to submit reporting to the CSSF on an annual basis.

We can support you at every step of the reporting process implementation and execution as well as when it comes to selecting reporting solutions.

Service suite

PwC has developed thematic solutions that will make your investment firm easier to understand and implement new prudential requirements.

Various training sessions specifically tailored to your needs. From general overview on the new framework to more tailored technical workshops on specific topics.

Assessment of the impact of the new prudential framework, including IFD, IFR as well as the guidelines from the European Banking Authority (EBA). From quantifying the impact on the capital or liquidity requirements to highlighting the changes required to internal governance and risk management practices, remuneration policy and set-up as well as regulatory reporting and disclosures.

Assistance in implementing the changes to your systems and processes to comply with the new prudential framework.

This operational assistance can cover:

- New calculations and methodologies development and implementation

- Governance model development

- Risk management and remuneration frameworks alignment

- Regulatory reporting update

- Disclosures development

- Project management support

- Subject Matter Expert support

Providing digital solutions covering regulatory reporting and disclosure requirements and, upon request, other capabilities, such as:

- Stress testing

- Budgeting and forecasting

- Management reporting / dashboarding

Contact us