The world needs globally accepted sustainability reporting standards to ensure transparent, comparable information for all stakeholders – businesses, investors, customers, employees, suppliers, regulators and governments. The quality of ESG reporting should be as high as it is for financial reporting and should be capable of being assured. This ensures a level of transparency and trust in the information that stakeholders are relying on.

One need look no further than the ISSB and GRI Memorandum of Understanding (MoU) for a clear indication of global alignment and a solid foundation for future ESG reporting.

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

What a hot topic ESG is. Even prior to the COVID-19 pandemic, the demand by stakeholders for environmental, social and governance (ESG) information was gathering steam. Now ESG has moved into the mainstream. In this blog, we focus on the role of ESG reporting, also known as sustainability reporting, and how it can ultimately lead to value creation for all stakeholders.

Regulators and standards setters are taking unprecedented action with speed, for example, in recent weeks we have seen the first draft Sustainability Reporting Standards from the IFRS Foundation’s new International Sustainability Standards Board, a 500+ page draft climate regulation from the United States’ Securities and Exchange Commission and the European Union’s draft sustainability standards are expected any day.

And these are all in addition to existing regulations such as The Sustainable Finance Disclosure Regulation (SFDR) which “represents quite possibly one of the most transformational regulatory developments in the history of Europe’s financial landscape”, according to PwC’s global sustainable finance specialists in 2022 – The growth opportunity of the century.They “expect ESG Mutual Funds assets to skyrocket to between EUR 5.4tn and EUR 7.6tn by 2025 – making up between 41% and 57% of total EU-domiciled Mutual Fund AuM”. And that’s just ESG Mutual Funds and just in Europe.

“One inescapable reality is that decarbonising the global economy is a monumental task, with far-reaching economic trade-offs that will challenge countries, industries, companies, and individuals,” according to PwC’s Global Investor Survey: The economic realities of ESG. “Another is the growing impact of the ESG movement, as it causes major investors, and the companies they hold in their portfolios, to rethink the risks of traditional business models, and the opportunities for more sustainable value creation in the future.”

Businesses and their investors are exploring the necessary transformation in business and operating models to secure the medium and long-term viability of their businesses – and they are balancing that with any necessary short-term implications for cash flow and profit.

Investors are catalysts for this kind of change – but they need quantitative and qualitative information about how resilient and sustainable their portfolio companies are. Currently, there is a lack of consistent, comparable reporting against a universal set of ESG metrics.

And what we no longer have is time to make excuses about this lack of comparable information. Studies and books like Ten Years to Midnight believe the solutions to the world’s most urgent challenges are within reach, but we only have a few years. We can no longer afford to ‘wait and see’.

We can change for the better by coming together

According to most dictionaries, convergence is when two or more things come together to form a new whole. Convergence has been needed in the ESG Reporting Ecosystem for more than a quarter of a century, but only now has it reached the point where stakes have never been higher. The next steps can make the difference between all parties contributing to sustainable outcomes, and disastrous outcomes for our society and the planet.

Bringing leaders together to chart a common path is precisely what occurred at a recent PwC event with the World Economic Forum, also known as the WEF. The event, for Asset Managers, closely followed insights on the latest developments in corporate reporting, including: the ISSB, GRI and the catalyst Stakeholder Capitalism project from the WEF, at the global level; and, in the EU, the Sustainable Finance Disclosure Regulation (SFDR) and the Corporate Sustainability Reporting Directive (CSRD).

The WEF convenes experts working to catalyse progress towards globally accepted ESG standards and to improve comparability of reporting for users, including asset managers. A main objective is to engage with asset managers on how this convergence is important for their ESG analysis and hear some of the latest research on what investors want.

Investors are crystal clear about the importance of ESG information

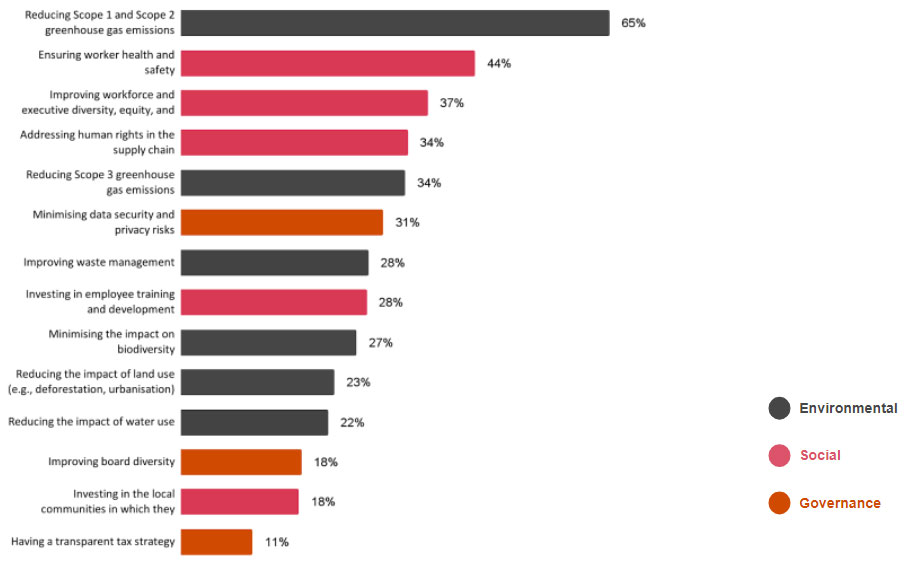

Investors are clear about the importance they attach to ESG, and it’s not just the climate that is a priority for them, it’s social matters as well – workforce health and safety, diversity and equality, and human rights in the supply chain are all top five priorities for them, according to PwC’s Global Investor Survey, conducted in September 2021 (see chart below). Around 325 investors were surveyed globally, the majority of whom were self-identified active asset managers making investments for the long term.

Broadly, those investors expressed commitment to ESG goals in their investing and as a priority for their portfolio companies. Tellingly, at the same time, 81% of respondents expressed reluctance to take a hit on their returns exceeding one percentage point in the pursuit of ESG goals. Let that sink in for a moment. It’s important to listen to what everyone at the table has to say, and mindsets are changing, but in the end, and taking the argument to the extreme, there is no profitable business on a dead planet.

Many respondents also described significant reservations about the quality of the information available to them when evaluating ESG priorities, including information on the carbon emissions of their investments.

Of the ESG issues listed below, which do you think are the most important for companies in the main industry you cover to prioritise*?

Base: (325) – Please note: due to rounding, percentages may not add exactly to 100% *respondents could select up to 5

What do investors think?

Responses to PwC Global Survey 2021

Source: PwC’s 2021 Global Investor Survey

All stakeholders agree: globally aligned standards are key

ESG Reporting standards and frameworks are essential tools to measure and manage priority ESG topics. They enable organisations to measure, manage, and communicate their exposure to ESG risks and opportunities, as well as their impacts on society and the planet, to inform strategy and provide accountability and transparency to stakeholders.

Over the past decade, various guidelines for ESG reporting have emerged, including voluntary standards, reporting frameworks, and national legislation. As a result, stakeholders struggle to access comparable information, leading to calls for globally aligned ESG reporting standards.

This would improve the comparability of information, as well as increase the quality of disclosure. More concretely, it would enable comparable reporting of performance against targets and investor allocation of capital to support sustainable business transitions.

Progress towards globally aligned ESG reporting has been faster in the last year than in the previous decade, and the establishment of the International Sustainability Standards Board (ISSB) is an important step in the right direction.

At the same time, regulators and governments around the world are taking action to help ensure that capital is targeted towards sustainable transition and that both investors and businesses are accountable for their societal and planetary impacts, as well as their immediate economic ones.

Global and EU standards are not ready – only exposure drafts are beginning to emerge – but that’s no excuse to delay.

ISSB signposts the major voluntary standards, including those identified in the WEF’s Stakeholder Capitalism Metrics (SCM), so that companies can report now on all relevant ESG topics to give stakeholders essential information and get ready for new standards which are being built on the existing voluntary standards.

The WEF’s SCM identify some of the most important universal topics and standards from existing standard setters, including SASB, the GRI, TCFD and others. In the WEF’s own words, “This set of 21 core and 34 expanded metrics and disclosures…are focused on four themes, People, Planet, Prosperity and Principles of Governance…[and they] reflect a six-month consultation process with more than 200 companies, investors and other interested parties.” They are CEO-led, investor supported and already tried and tested by companies around the world.

What we witnessed at the WEF event is that investors are becoming more and more aware of what’s at stake, and where the benefits lie.

To give you a sense of this, here are some snippets of what was said:

“…if a company is assuring certain metrics, and even striving for reasonable assurance, you know that they are really interested in using those metrics for managing their business and also to communicate their performance.” “You could look at ten financial indicators and you would have a pretty good idea of the financial health of that company … you could look across a portfolio and pretty much understand by looking at sales and margins, and cash flow and leverage etc what a company’s performance was like.” “The trouble with ESG data is we don’t have that, we don’t have data for half of the supply chain, particularly as you move into mid and small sized companies…So, we’ve got to recreate for ESG what we have for financial data to bring ESG data into the mainstream.”

Companies that are part of the WEF coalition and adopting the recommended metrics to catalyse progress to global ESG standards, have identified multiple benefits, which are:

Active CEO buy-in and support for progressing their organisation’s globally comparable sustainability reporting and enacting change within an organisation (up-front investment that will reduce cost and simplify reporting in the long term);

Meeting investor and stakeholder demands for comparable ESG information ahead of global regulations;

Building trust and accelerating positive stakeholder outcomes;

Improved ability to demonstrate ESG performance and progress among peers;

Contributing to the collective business voice that’s driving standard setter convergence;

An all important seat at the table to provide input to emerging international sustainability standards.

Calls to action. Everyone has a role to play!

We believe there is a role for all stakeholders to bring about convergence and change.

Investors and companies must proactively engage in the global, regional and national standard-setting processes to ensure they are meaningful, feasible to implement, identical ( where they can be) and that they result in globally well understood and comparable disclosures and metrics. It simply won’t work to “wait and see” until the new standards are required, and then discover they are too difficult to implement or the information they provide isn’t useful.

Companies can immediately align at the universal level (industry agnostic) by adopting the WEF SCMs, if they have not already done so. This shows that ESG is taken seriously by management and demonstrates a willingness to proactively improve the quality and comparability of information for stakeholders; it also helps companies prepare for emerging ISSB standards and regional or territory regulations.

Investors can encourage their portfolio companies to use the core WEF SCMs – either to get started, or to ensure the companies they are investing in aren’t remaining silent on what is clearly a vital topic. They can use SCM information to help allocate capital and steward businesses towards sustainable transition.

Standard setters, governments and regulators, should continue the path of convergence. Alignment simply isn’t enough. Standards on the same topic will ideally be identical at global, regional and national levels to avoid cost, confusion, and a lack of comparability.

What we think

Steven Libby, PwC EMEA Asset & Wealth Management Leader

Together with the WEF, we continue to work to bring all parties together to support globally aligned standards. As investors continue to call on their portfolio companies to provide comparable ESG information, we encourage use of the emerging standards from the ISSB, as well as existing standards on priority topics, such as those identified in the WEF SCM.

Nadja Picard, Partner, Global Reporting Leader at PwC

As companies consider their most material topics and look for help, they can use the WEF Stakeholder Capitalism Metrics as a starting point for their ESG reporting, this readies them for emerging standards and regulation, aligns them with other companies globally and immediately improves the comparability of their reporting for investors and other stakeholders.